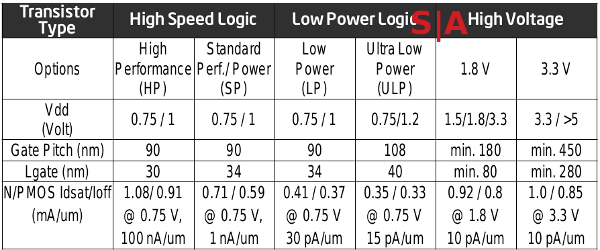

SOITEC & MBDA purchased Dolphin Integrated a 22FDX/FDXcelerator partner. They have also designed on STM's 28FD.

“Dolphin Integration represents a strategic opportunity for Soitec to reinforce a full IP and service offering related to energy efficient solutions for chip design on FD-SOI. This is a major differentiating factor for FD-SOI and a key accelerator of FD-SOI adoption in major market segments,” highlighted Paul Boudre, CEO of Soitec.

“MBDA investment will strengthen the French defense industrial base since it will provide Dolphin Integration with a more stable flow of defense related revenues and a closer technological collaboration that will allow it to enhance the access of its specialized microelectronics offering to the entire French and European defense industry,” said Antoine Bouvier, CEO of MBDA.

MBDA is jointly owned by Airbus (37.5%), BAE Systems (37.5%), and Leonardo (25%).

AirBus seems to be 110nm to 45nm, with works on FD28 via DAHLIA.

BAE 45nm =>

https://www.baesystems.com/en-us/ou...uct-sites/space-products-and-processing/asics

I'm going to assume Leonardo is the same.

I guess at this point, the best thing to do would be to compare GF to other semiconductor fabricators who don't push leading-edge nodes anymore. How often do they update their nodes?

Based on UMC with comparable technology:

28nm HPM -> 2013

28nm HPC -> 2014

28nm HPCU -> 2016

28nm HPCU+ -> 2H 2017/1H 2018

22nm ULP -> 2H 2018/1H 2019

"Chipmaker UMC expects to introduce 22nm process technology as early as 2018, DigiTimes reports, citing comments made at its investors meeting. The company, which began shipping 14nm chips in Q1, has started IP development for its 22nm process, and plans to introduce the node technology in 2018 or 2019."

-

https://thefly.com/landingPageNews.php?id=2542205

"Both 28nm and 22nm process technologies will be the future focus of United Semi, said Chien, adding that the 12-inch foundry is looking to expand its client portfolio and deliver economies of scale as soon as possible.

Monthly production capacity at United Semi is set to reach 25,000 wafers for its first phase of expansion, Chien disclosed.

...

United Semi will build additional production capacity according to customer demand, and will not "blindly" expand capacity, Chien noted."

-

http://www.simmtester.com/page/news/printerFormat.asp?num=20185&rnd=163590714670217090

=> Fab 12X maxes at 50,000.

"14nm accounted for 2% of 4Q17 revenue, while 28nm contribution remained at 15%."

https://www.businesswire.com/news/home/20180124005487/en/UMC-Reports-Fourth-Quarter-2017-Results

=> Fab 12X is ramping up.

Most recent:

"Business from 14nm increased to 3% of 2Q18 revenue, while 28nm contribution was 15%."

https://www.businesswire.com/news/home/20180725005300/en/UMC-Reports-Quarter-2018-Results

~1% every two quarters. Hopefully.

28nm ramped up fast:

https://www.eetimes.com/document.asp?doc_id=1326479

1% to 9%...

“A normal ramp would be three to four quarters to get to 20% of revenue, and you’ve already been ramping for four quarters, and it’s only 9% of revenue,” Heyler said."

Normal would be 20%, oof.

So, if revenue was broken down:

"IC Insights, a company that tracks semiconductor data, estimates that GlobalFoundries had $6 billion in revenue in 2017, although it does not break that down in terms of profit."

-

https://www.sfchronicle.com/busines...lFoundries-profitable-Yes-and-no-12906650.php

Add that with:

https://www.globalfoundries.com/new...-billion-design-win-revenue-22fdxr-technology

https://www.semiwiki.com/forum/content/7604-fdsoi-status-roadmap.html

One sixth of their revenue was from 22FDX which is 16% of the revenue being FDSOI. 22FDX began in Q1 2017(Validated: Ramp2HVM 2H 2017) and by Q2 2018 had $2 billion USD. So, this year should be $7 billion in revenue. $1 billion in the first half and $1 billion in the second half with pessimistic results.

22FDX is aggressively following historic trends. Which 28nm and 14nm at UMC did not even though they had DDC a competitor of FDSOI on 28nm.

"TSMC is expected to have almost 6x the sales volume at <40nm as compared to GlobalFoundries in 2016 ($15.6 billion for TSMC and $2.6 billion for GlobalFoundries)."

https://electroiq.com/2016/09/leading-edge-leads-the-way-in-pure-play-foundry-growth/

22FDX is basically on par with the entirety of <40nm from 2016 within four quarters. Competition hasn't really even started yet either:

- 22nm ultra-low power (22ULP) technology was developed based on TSMC’s industry-leading 28nm technology and is expected to start production in the second half of 2018.

- 22ULL technology targets the IoT and wearable devices applications and is expected to start risk production in the second half of 2018.

That is with SOITEC B2 @ 100K per year.

PDSOI(also 3D-FD) is being swapped to FDSOI for 350K(400K) wafers per year (2018 -> 2019).

By 2020, the facility will be 800K w/ 650K for 2D-FD and 150K for other.

"Consequently, Soitec expects its Bernin II production site to reach a capacity utilization rate close to 100% towards the end of FY'19 or the beginning of FY'20."

Singapore will qualify in 1H 2019, then by 2H 2019/2020 will also have 800K wafers per year.

There is also plans for a third plant with 1M per year.

8000 wpm (now) -> 33,000 wpm (later1) -> 54,000 wpm (later2)

If demand keeps up would the $2B become <$8B at later1 and <$13B at later2. Then, there is 12FDX which would be a higher revenue source in late 2020 to early 2021. This is ignoring GF Chengdu and SOITEC Singapore, and if GF's Singapore and Malta jump in. Also ignoring extended SOITEC sources/licensees like SEH and GlobalWafers.