-

We’re currently investigating an issue related to the forum theme and styling that is impacting page layout and visual formatting. The problem has been identified, and we are actively working on a resolution. There is no impact to user data or functionality, this is strictly a front-end display issue. We’ll post an update once the fix has been deployed. Thanks for your patience while we get this sorted.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Discussion AMD 2024-Q4 Earnings

Page 2 - Seeking answers? Join the AnandTech community: where nearly half-a-million members share solutions and discuss the latest tech.

What jumped out at me is Dell...ummm no that's not right, Hell, yes, Hell froze over.

I choose to think this is more collateral damage from raptor lake.Dell and AMD announced that AMD Ryzen AI PRO processors will power new Dell Pro notebook and desktop PCs, bringing exceptional battery life, on-device AI, Copilot+ experiences and dependable productivity to enterprise users. For the first time, Dell will offer a full portfolio of commercial PCs based on Ryzen processors, marking a significant milestone in the companies' collaboration.

Market doesn't care about incremental growth, since AMD isn't growing like Nvidia was in AI, down it goes lol

Yeah, I think this is more about Q1 projections than Q4 performance as AMD met/slightly exceeded Q4 expectations. It seems investors keep wanting AMD to have an NV moment where the revenue just does a crazy jump quarter after quarter, but AMD's growth as the follower in the segment as been more incremental in comparison. I couldn't listen to the call so it will be interesting to read the discussion around DC GPU revenue going forward. It will also be interesting to see NV's projections as it had started to show a plateauing in revenue as well in the 2H of the year.

desrever

Senior member

In the call, Lisa basically said that H1 2025 is going to be flat for DC GPU and H2 will significant growth.Yeah, I think this is more about Q1 projections than Q4 performance as AMD met/slightly exceeded Q4 expectations. It seems investors keep wanting AMD to have an NV moment where the revenue just does a crazy jump quarter after quarter, but AMD's growth as the follower in the segment as been more incremental in comparison. I couldn't listen to the call so it will be interesting to read the discussion around DC GPU revenue going forward. It will also be interesting to see NV's projections as it had started to show a plateauing in revenue as well in the 2H of the year.

She implies companies are waiting for MI350 which will ramp mid year.

In the call, Lisa basically said that H1 2025 is going to be flat for DC GPU and H2 will significant growth.

She implies companies are waiting for MI350 which will ramp mid year.

That doesn't sound bad to me at least, lol.

In the call, Lisa basically said that H1 2025 is going to be flat for DC GPU and H2 will significant growth.

She implies companies are waiting for MI350 which will ramp mid year.

There is also an elephant in the room - which is that AMD can't get enough (if any) HBM3e for Mi325x.

Samsung and I believe also Micron have delays. AMD needs 12-high stacks of HBM3e, which is even more rate than HBM3e 8-high. for Mi325. There was a news story yesterday that Samsung just past NVidia qualification for HBM3e 8-high, so it is unlikely that Samsung is shipping any 12-high stacks.

Pretty big news from the conference call:

And then the big news is on the MI350 series. So we had previously stated that we thought we would launch that in the second half of the year. And frankly, that bring-up has come up better than we expected, and there is very strong customer demand for that. So we are actually going to pull that production ramp into the middle of the year, which improves our relative competitiveness.

That doesn't sound bad to me at least, lol.

Maybe I am reading too much into this, but I have a feeling that AMD has additional customers for Mi350. And / or bigger deployments with existing ones.

One thing to keep in mind is that Blackwell in N4, while Mi350 will likely be N3. Plus optimizations, plus support for smaller data types. So it will likely narrow the gap with NVidia.

There is also an elephant in the room - which is that AMD can't get enough (if any) HBM3e for Mi325x.

Samsung and I believe also Micron have delays. AMD needs 12-high stacks of HBM3e, which is even more rate than HBM3e 8-high. for Mi325. There was a news story yesterday that Samsung just past NVidia qualification for HBM3e 8-high, so it is unlikely that Samsung is shipping any 12-high stacks.

AMD has been working with Samsung to qualify HBM3e memory for a while now. Not positive that it's ready (they did launch so I assume it's ready) and I may be misremembering, but I think AMD wasn't trying to push as fast of clocks as NV and so was having an easier time getting it qualified.

Maybe I am reading too much into this, but I have a feeling that AMD has additional customers for Mi350. And / or bigger deployments with existing ones.

Yes, they said that DC GPU should be significantly higher in 2H25 than in 4Q24, so they will need additional customers/deployments to make that happen.

AMD has been working with Samsung to qualify HBM3e memory for a while now. Not positive that it's ready (they did launch so I assume it's ready) and I may be misremembering, but I think AMD wasn't trying to push as fast of clocks as NV and so was having an easier time getting it qualified.

That would certainly be good news. But now with Mi350 being pulled in, the window for Mi325 likely narrowed. A bit of a pickle for AMD in near term, but longer term, AMD may more than make up for it with faster adoption of Mi350

That would certainly be good news. But now with Mi350 being pulled in, the window for Mi325 likely narrowed. A bit of a pickle for AMD in near term, but longer term, AMD may more than make up for it with faster adoption of Mi350

Depending on how the costs shake out, there very well could be a market for MI325 after MI350 launches as it gets very close to the total RAM.

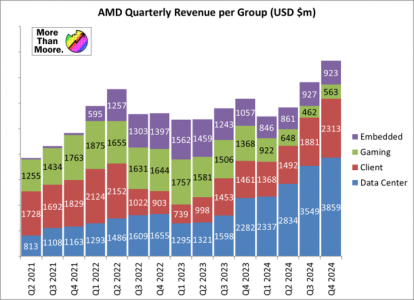

Here are some stats on client in Q4:

Intel Q3 to Q4:

Revenue: $7.3 -> $8.0

Market share: 79.3% -> 77.7%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 22.3%

Now, Intel stated that it sold meaningfully less in Q4 than in Q3 (say 5%) and then stuffed additional 9% into the channel. So than, what was sold through by Intel was $7 billion. In comparison, Lisa said sell through was excellent. Adjusting the numbers to only what sold through

Intel Q3 to Q4:

Revenue: $7.3 -> $7.0

Market share: 79.3% -> 75.3%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 24.7%

In other words, AMD may have gained 4% in client in a single quarter.

Intel Q3 to Q4:

Revenue: $7.3 -> $8.0

Market share: 79.3% -> 77.7%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 22.3%

Now, Intel stated that it sold meaningfully less in Q4 than in Q3 (say 5%) and then stuffed additional 9% into the channel. So than, what was sold through by Intel was $7 billion. In comparison, Lisa said sell through was excellent. Adjusting the numbers to only what sold through

Intel Q3 to Q4:

Revenue: $7.3 -> $7.0

Market share: 79.3% -> 75.3%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 24.7%

In other words, AMD may have gained 4% in client in a single quarter.

Here are some stats on client in Q4:

Intel Q3 to Q4:

Revenue: $7.3 -> $8.0

Market share: 79.3% -> 77.7%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 22.3%

Now, Intel stated that it sold meaningfully less in Q4 than in Q3 (say 5%) and then stuffed additional 9% into the channel. So than, what was sold through by Intel was $7 billion. In comparison, Lisa said sell through was excellent. Adjusting the numbers to only what sold through

Intel Q3 to Q4:

Revenue: $7.3 -> $7.0

Market share: 79.3% -> 75.3%

AMD Q3 to Q4

Revenue: $1.9 -> $2.3

Market share: 20.7% -> 24.7%

In other words, AMD may have gained 4% in client in a single quarter.

For client they are just back where they were 30 months ago, that s the graph from Ian Cutress, one has to wonder what happened in Q3 2022 - Q2 2023 despite launching Zen 4, they had a set back even for servers despite a superior offering.

Attachments

For client they are just back where they were 30 months ago, that s the graph from Ian Cutress, one has to wonder what happened in Q3 2022 - Q2 2023 despite launching Zen 4, they had a set back even for servers despite a superior offering.

True, but in the span of those 30 months, AMD client revenue dropped at one point down 67% in Q1 2023 (for reasons). So this is not a straight line.

For client they are just back where they were 30 months ago, that s the graph from Ian Cutress, one has to wonder what happened in Q3 2022 - Q2 2023 despite launching Zen 4, they had a set back even for servers despite a superior offering.

There was a rush to buy chips during the pandemic due to supply chain fears. Then, when things started to mellow out, companies realized they over bought and cut back spending dramatically. Intel got hit pretty hard too during this time frame but then they used their leverage to push a bunch of cheap RPL chips into the channel to increase sales as much as they could.

When AMD has more than 50% of the markets where they compete with Intel, that will be when Intel is the underdog. 😉I remember hating Dell with a passion because they wouldn't make AMD K6-2/3 and Athlon systems. If I were a noob again, I might gravitate towards Intel(under dog), and that gives me conflicting feelings.

Dell has been suffering mass layoffs and is slipping further behind HP and Lenovo. They were undoubtedly the unnamed partner that had millions of defective raptor lake CPUs, that was being reported on. With Intel being unable to offer the performance, incentives, and level of services, compounding the historic SNAFU. (Info is from the news concerning Intel SMG layoffs and restructuring) there is no better time to start doing some real biz with AMD.

On a humorous note: I'd like to congratulate PC on winning the console wars. 🤪

Yay, I am due for a new laptop at work in the spring this year, we are using Dell only, not sure why but gut feeling tells me the AMD skus will arrive just after I get assigned another Intel furnace...What jumped out at me is Dell...ummm no that's not right, Hell, yes, Hell froze over.

Yay, I am due for a new laptop at work in the spring this year, we are using Dell only, not sure why but gut feeling tells me the AMD skus will arrive just after I get assigned another Intel furnace...

Me too! But even though they use HP, I expect it to be Raptor. But it could be Hawk.

Looking at those two graphs Mercury Research numbers were, and still are, for sale, Intel s halved volume sales since 2021 dont match what seems made up numbers from this firm.

www.computerbase.de

www.computerbase.de

Server-Prozessoren: Intel Xeon mit niedrigstem Absatz in 14 Jahren

Jetzt haben die Absatzzahlen von Intel Xeon einen neuen Tiefpunkt erreicht – den tiefsten innerhalb der letzten 14 Jahre.

Flat here means what? Compared to H1 a year ago or to current sales levels?In the call, Lisa basically said that H1 2025 is going to be flat for DC GPU and H2 will significant growth.

She implies companies are waiting for MI350 which will ramp mid year.

TRENDING THREADS

-

Discussion Zen 5 Speculation (EPYC Turin and Strix Point/Granite Ridge - Ryzen 9000)

Discussion Zen 5 Speculation (EPYC Turin and Strix Point/Granite Ridge - Ryzen 9000)- Started by DisEnchantment

- Replies: 25K

-

Discussion Intel Meteor, Arrow, Lunar & Panther Lakes + WCL Discussion Threads

- Started by Tigerick

- Replies: 25K

-

-

-